Renewable energy brings California emissions below 1990 levels

The U.S. state’s latest report shows that it has beat its 2020 target for emissions reductions four years early, mostly thanks to more renewable energy.

The nuclear industry’s substantial propaganda machine has spilled much ink in claiming that renewable energy has not resulted in meaningful reductions in greenhouse gas (GHG) emissions. In particular, nuclear advocates have pointed to Germany, where power sector emissions and shares of coal generation have declined slowly, despite large amounts of renewable energy going online, due in part to the simultaneous nuclear shutdown.

Germany can make its own arguments for the Energiewende, which has other goals that preceded GHG reduction. However, it is not the only region that is undergoing an energy transition. The latest data from California shows a much more clear relationship between ongoing deployment of renewable energy and reduction in emissions, despite the closure of one of the state’s last nuclear power plants.

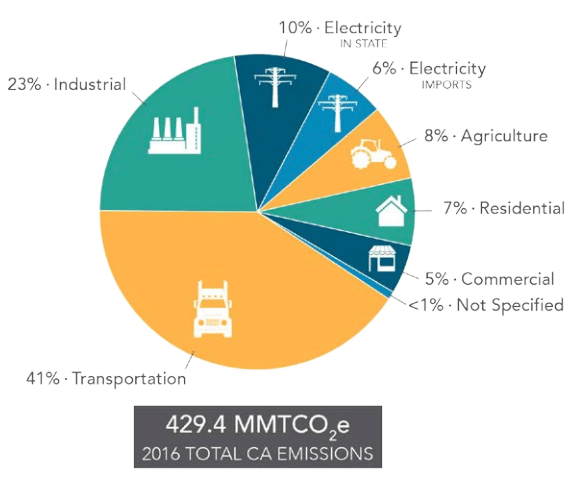

Last week the California Air Resources Board (CARB) announced that the state’s GHG emissions had fallen to 429 million metric tons in 2016. This is below the 431 metric tons emitted in 1990 for the first time this century, and as such beats the state’s goal for emissions reductions four years early.

<p> <span style="font-weight: bold;">Learning curve</span><br />

The latest ITPRV concludes that PV manufacturing continues to deliver around a 21% decrease in average selling price (ASP) for every doubling of PV production capacity. This rate has deviated in accordance with the tremendous market fluctuations between 2003 and 2013, however the average linear price digression still holds.<br />

The most recent data points on the learning curve graph indicate that with 34 GWp of production capacity in 2013, ASPs came in at US$0.72/W. In 2013, with 39.3 GWp of capacity, ASPs averaged $0.62/Wp.<img style="width: 528px; height: 351px;" src="fileadmin/PVI_website_pictures/SEMI_spot_prices.png" txdam="20277" alt=" /><br />

Looking more deeply at recent ASP decreases, the roadmap finds that between 2010 and 2015, <a class="gco-link" href="https://www.pv-magazine.com/pv-taiwan-oversupply-remains-an-issue">manufacturing overcapacity</a> continues to play a major role. The ITPRV concludes that with over 60 GWp of module capacity remaining in the market and exceeding demand, predicted in the report, of 50 GWp, pressure on PV module manufacturing will persist. To survive such pressures, the roadmap finds that manufacturers will have to continue to focus on reducing consumable and materials costs.<br />

To meet the challenge presented by overcapacity, the ITPRV proffers three strategies for manufacturers:<br />

i) Continue the cost reduction per piece along the entire value chain by optimizing the utilization of the installed production capacity and by using Si and non-Si materials more efficiently. ii) Introduce specialized module products for different market applications (i.e. tradeoff between cost-optimized, highest volume products and <a class="gco-link" href="https://www.pv-magazine.com/niche-solar-products-enjoying-their-moment-in-sun">fully customized niche products</a>). iii) Improve module power/cell efficiency without significantly increasing processing costs.</p>

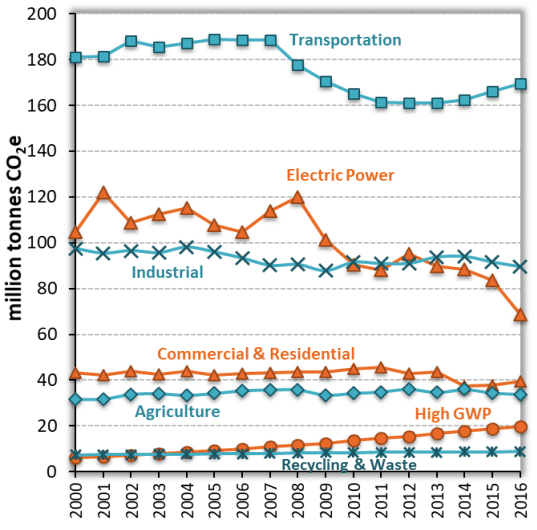

” data-medium-file=”” data-large-file=”” />In line with previous reports, a detailed inventory by CARB shows that this was largely due to deployment of renewable energy. Overall emissions fell 18% in 2016 alone and total electric power emissions have fallen by roughly 1/3 from over 100 million tons CO2 equivalent in 2000 to less than 70 million tons in 2016.

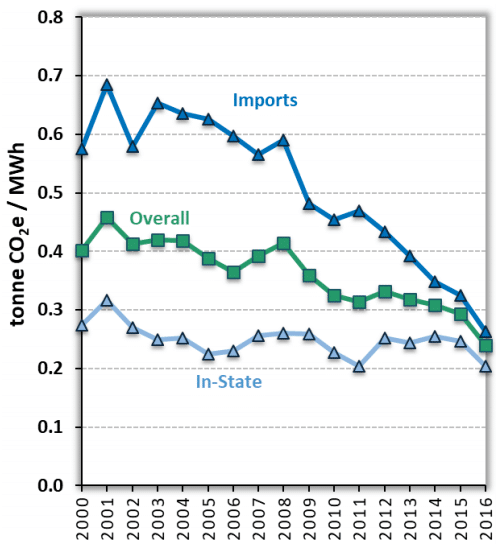

Some of the progress in 2016 and 2017 has been due to very heavy hydroelectric generation, but the overall trend also shows a decline, and the biggest decreases from 2010-2016 came from lower GHG from imports. This shows particularly strongly in GHG intensity figures.

And as pv magazine has previously reported the publicly available data on the source of these imports is incomplete, making it difficult to independently validate CARB’s assessments. However, data from California Energy Commission compiled by Joe Deely shows that the declared share of nuclear power in the state’s energy mix has not increased meaningfully since 2013, while solar and hydro have increased substantially.

The big picture of decarbonization

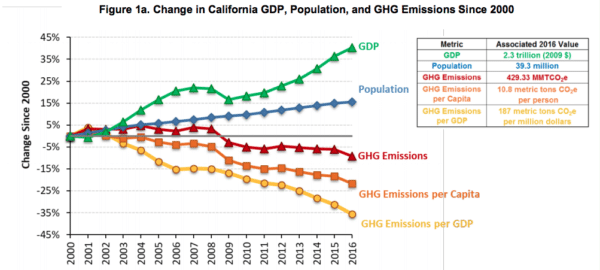

One of the fascinating aspects of California’s emissions reductions is that the state is beating its goals to bring down emissions while its population and gross domestic product (GDP) both grow. Overall emissions per capita have fallen by roughly 1/4, and emissions per unit of GDP by about 1/3, with a clear decoupling of emissions from GDP starting in the year 2003.

This is not to say that the recession had no role. California’s transportation emissions fell during the 2008 recession and have not returned to their 2007 levels since. Residential emissions have also fallen in recent years, however this has merely mirrored the number of heating days, indicating little meaningful progress in energy efficiency.

For California to make further progress in emission reductions, it will not be enough to only deploy renewable energy. Nearly 2/3 of the state’s emissions currently come from the transportation and industrial sectors, and in particular it will be key to electrify transportation and/or implement transit, housing and land use policies that provide alternatives to the lengthy automobile commutes that are the norm in many of the state’s urban areas.

The latter may be particularly thorny, given the NIMBY resistance to denser housing by affluent homeowners that frequently features in the politics of cities such as San Francisco and Berkeley.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

Christian Roselund served as US editor at pv magazine from 2014 to 2019. Prior to this he covered global solar policy, markets and technology for Solar Server, and has written about renewable energy for CleanTechnica, German Energy Transition, Truthout, The Guardian (UK), and IEEE Spectrum.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

pv magazine Australia offers bi-weekly updates of the latest photovoltaics news.

We also offer comprehensive global coverage of the most important solar markets worldwide. Select one or more editions for targeted, up to date information delivered straight to your inbox.

The cookie settings on this website are set to "allow cookies" to give you the best browsing experience possible. If you continue to use this website without changing your cookie settings or you click "Accept" below then you are consenting to this.

Some of the progress in 2016 and 2017 has been due to very heavy hydroelectric generation, but the overall trend also shows a decline, and the biggest decreases from 2010-2016 came from lower GHG from imports. This shows particularly strongly in GHG intensity figures.

Some of the progress in 2016 and 2017 has been due to very heavy hydroelectric generation, but the overall trend also shows a decline, and the biggest decreases from 2010-2016 came from lower GHG from imports. This shows particularly strongly in GHG intensity figures.

For California to make further progress in emission reductions, it will not be enough to only deploy renewable energy. Nearly 2/3 of the state’s emissions currently come from the transportation and industrial sectors, and in particular it will be key to electrify transportation and/or implement transit, housing and land use policies that provide alternatives to the lengthy automobile commutes that are the norm in many of the state’s urban areas.

For California to make further progress in emission reductions, it will not be enough to only deploy renewable energy. Nearly 2/3 of the state’s emissions currently come from the transportation and industrial sectors, and in particular it will be key to electrify transportation and/or implement transit, housing and land use policies that provide alternatives to the lengthy automobile commutes that are the norm in many of the state’s urban areas.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.