From pv magazine print edition 11/24

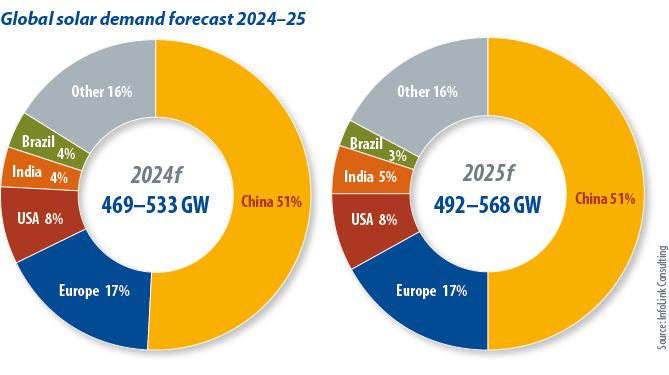

Economic fluctuations and policy changes have led to a slowdown in global solar market growth in the second half of 2024. InfoLink forecasts solar demand to reach up to 568 GW in 2025, growth of 7% compared to up to 533 GW in 2024.

China will continue to lead solar deployments, with ground-mounted sites comprising 60% of demand. Projects delayed by land approvals, grid balancing, and power rationing are expected online in late 2024 and the first half of 2025.

Small-scale, “distributed” solar arrays could be undermined by policy uncertainty, as the government has pledged a new power market trading system in 2024. Rooftop rental costs are also rising. InfoLink said it expects Chinese demand to stay flat from the 240 GW to 260 GW expected in 2024, to between 245 GW and 265 GW in 2025.

In 2024, the United States removed a tariff exemption for imported bifacial PV modules and also raised Section 301 tariffs on Chinese solar cells and modules from 25% to 50%. The US Department of Commerce launched antidumping and countervailing duty (AD/CVD) investigations into cells and modules from Cambodia, Malaysia, Thailand, and Vietnam with preliminary rulings expected in November 2024. Southeast Asian solar manufacturers are awaiting the AD/CVD rulings and expect them to drive higher solar project development costs.

US policy

Election-related uncertainty about whether US Inflation Reduction Act subsidies will continue has seen ground-mounted projects stall, with demand expected to recover only from 2025 onwards. InfoLink expects annual US demand growth of 10% to between 38 GW and 44 GW in 2025. US distributed PV demand is weak after leading solar state California’s NEM 3.0 net-metering legislation reduced the amount paid for electricity exported to the grid from domestic solar arrays.

European uncertainty

Despite grid capacity constraints, European solar generation has driven frequent negative electricity prices in 2024 but big PV markets like Germany and Spain have experienced economic stagnation and delays in ground-mounted projects. Potential subsidy scheme adjustments are further clouding market sentiment.

The European Union wants to foster domestic solar manufacturing and has introduced the Net-Zero Industry Act, Critical Raw Materials Act, and anti-forced labor rules to back that aim. Subsidy measures remain unclear, however, and European production capacity cannot meet demand.

InfoLink expects European solar demand to rise 9% to 10% in 2025, up from an expected 77.4 GW to 85 GW in 2024, to hit 85 GW to 93 GW. Incentives, European policy, and member-state economic situations will be key to solar demand.

India rising

India’s PV installations are driven by government projects, including auctions for solar parks, rooftop panels, and agrivoltaics. Most aim for installation by 2026, making a 2025 installation rush likely. InfoLink expects India’s 2025 module demand to reach 25 GW to 35 GW, representing a 25% to 40% increase from 20 GW to 25 GW in 2024.

The Approved List of Models and Manufacturers (ALMM) legislation for modules was reinstated in April 2024, requiring government projects to use domestic modules from manufacturers on the list. Indian module production capacity is expected to meet demand. The ALMM for cells is set to be implemented in April 2026, meaning that, by then, government projects will be restricted to using modules assembled with Indian-made cells.

While module production capacity will be sufficient, cell output is facing challenges, as some Indian manufacturers lack adequate technological reserves, preventing large-scale expansion in the short term. Additionally, despite India’s 25% Basic Customs Duty on Chinese cell imports, the majority of domestic module manufacturers still rely heavily on Chinese cells, especially with falling prices in the Chinese supply chain in 2024. The Indian government aims to achieve full domestic manufacturing of both cells and modules by 2026 to meet growing local solar demand, but achieving that remains a challenge.

Brazil reduces quota

Brazil, a solar market dominated by distributed-generation projects, has benefited from the recent drop in Chinese module prices and from lower interest rates. Brazil included small PV projects in its Special Infrastructure Development Incentive Regime in the first half of 2024, enabling developers to benefit from partial tax exemptions for up to five years. As a result, Brazil’s solar demand in 2024 is expected to reach between 16.5 GW and 18 GW.

However, the Brazilian government announced a gradual reduction in the tax-free import quota for modules in July 2024. Quotas are expected to decrease between 2025 and 2026. Any imports exceeding the quota will be subject to a 10.8% tariff. Due to Brazil’s shortage of domestic module production capacity, developers will have to use imported modules with added tariffs, raising project costs. That will impact Brazil’s distributed-generation sector and may hinder demand growth in the long term. InfoLink forecasts that Brazil’s solar demand in 2025 will come in at 15.5 GW to 17 GW, down 5% to 6% year on year.

Global transition

Beyond 2025, political and economic factors pose challenges to the global solar industry, making it difficult for market demand to maintain the high growth rates seen in 2023 and 2024.

Despite weakening growth momentum, solar power remains the most cost-effective renewable energy technology on the market. Its excellent sustainability claims and potential for technological innovation provide strong momentum for future development.

About the author: Jonathan Chou is an assistant analyst in InfoLink’s solar research team. He previously supported research projects at an incorporated foundation. Chou focuses on regional policy research, monitoring project progress, and helping analysts compile information on global market movements and demand.

About the author: Jonathan Chou is an assistant analyst in InfoLink’s solar research team. He previously supported research projects at an incorporated foundation. Chou focuses on regional policy research, monitoring project progress, and helping analysts compile information on global market movements and demand.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.