Weekend read: Prospects for bifacial and large-format products

The pandemic and accidents at polysilicon labs in China’s Xinjiang region put PV manufacturers under pressure to maintain production this year, while slowing cell and module R&D. After half-cut and multi-busbar becomes commonplace, manufacturers will continue to explore the high-density assembly methods that emerged last year, as well as n-type cells. But the market is also shifting to large formats, and the share of bifacial products is growing this year. As sizing up modules can bring immediate returns, PV InfoLink’s Amy Fang expects the PV industry to prioritise the development of large formats and bifacial products next year.

Covid-19 to wreck economics of new solar and wind projects

While the full extent of the impact of the Covid-19 pandemics on the renewable energy market is yet to reveal itself, Norwegian consultancy Rystad Energy predicts new solar and wind projects will grind to a halt this year and experience a ripple effect in the years beyond as currencies across the globe continue to fall against the US dollar.

Short-term symptoms

The COVID-19 outbreak has disrupted the global PV supply chain. China, the largest manufacturing hub for solar products, has postponed factory openings in many regions, as it has been hit by logistical hiccups, staff shortages, and delivery delays. Manufacturers in some Chinese provinces are running under capacity, while those overseas are facing the same situation.

On prices, technology and 2019 trends

A maturing PV market does not automatically deliver certainty in terms of technology roadmaps and industry dynamics. Crystalizing trends and anticipating developments is the business of analysts, so pv magazine assembled four of solar’s best to talk about prices, technology and market-defining policy developments.

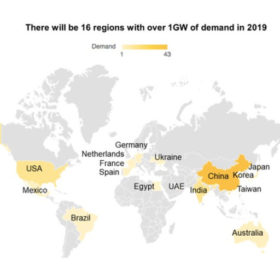

PV Info Link expects solar demand to reach 112 GW in 2019

That would mean a market increase of around 25% on this year. Demand is predicted to become particularly strong in the second half of the year. Australia is forecast to see lower demand than usual in the first quarter, but also be among 16 nations worldwide that will add over 1 GW of solar capacity in 2019.

Prices for monocrystalline solar modules are picking up

Analysts at Taiwan-based EnergyTrend and China’s PV Infolink have reported a further increase in demand for monocrystalline solar cells and modules in recent days. Their respective analyses on multi-crystalline products, however, do not match.

PV Info Link: Mono-cSi cell price drops below multi

According to PV Info Link, the price for monocrystalline cells in China fell below that of the usually cheaper multicrystalline products. However analysts expect it to be a blip, with multi prices expected to fall and mono to be supported by the Top Runner Program, now China’s main source of demand for the rest of 2018.

Module prices continue to fall

The latest reports from analysts at PV InfoLink and EnergyTrend show prices continuing to fall, though at a slower rate than was seen immediately after China’s 31/5 announcements. High efficiency mono-PERC modules fell to around $0.32/W, while multicrystalline module prices hold steady between $0.26 and $0.29/W.