The overall stationary battery energy storage market has had a strong year of development, illustrated by 83% more completed projects than in 2017. Project delays in 2017 meant more than 850 MW was completed in Q1 2018 – a strong start to the year. Project activity slowed in the second quarter, before rebounding in the third quarter, with almost 800 MW commissioned. The lowest number of projects were completed in the fourth quarter, owing to the traditionally slow winter and Christmas period.

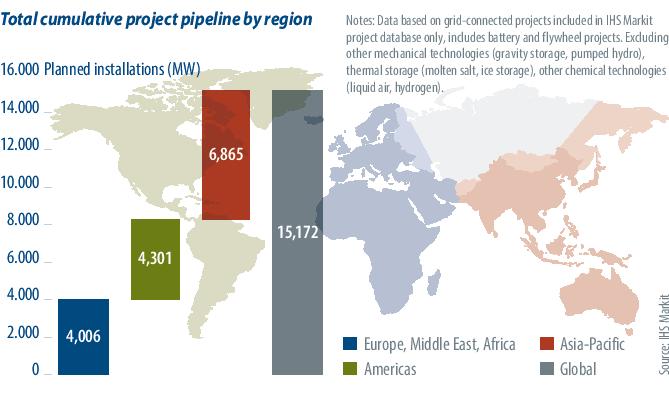

There is a positive future for battery energy storage, as the project pipeline continues to grow, reaching 15.2 GW at the start of 2019, which is half the size of the pipeline for new pumped hydro energy storage (PHES). Asia Pacific has the strongest pipeline, but it includes some speculative projects that – were they to be completed – would dwarf the current world’s largest single-site energy storage projects.

With the U.S. market poised for exponential growth in 2019, the Americas already have a project pipeline of over

4.3 GW. As policy frameworks advance across the United States, IHS Markit already tracks project activity in 39 states, which have operational energy storage systems, with an additional five states with projects planned or under construction.

Competitive landscape

NEC Energy Solutions, Nidec, and Tesla Energy were the leading energy storage system integrators in 2018 in terms of total megawatts commissioned, based on projects larger than 1 MW. Narada and Tesla Energy joined LG Chem and Samsung SDI as the most significant battery suppliers for projects commissioned, with these four companies also collectively accounting for 67% of the planned battery energy storage pipeline with confirmed suppliers.

A clear trend in 2018 was the increasing size of large front-of-the-meter systems, further proof the industry is maturing. Announcements for systems over

100 MW are occurring more frequently. While currently accounting for only around one third of total installations, behind-the-meter activity is increasing, highlighting the future importance of residential and commercial applications.

South Korean fires

During 2018 more than 15 battery fires were reported in South Korea, resulting in actions taken by the Ministry of Commerce, Industry and Energy (MOCIE). There are now more than 1,250 battery energy storage systems installed in the country. Following the increasing number of fires in the country, authorities prioritized conducting safety checks on all installed battery systems. A specialist taskforce worked alongside major battery manufactures and utilities to conduct inspections. As fires continue to occur in 2019, MOCIE announced a forced shutdown of 342 public energy storage systems and recommended that private owners of energy storage systems take them offline, until the ongoing investigation concluded. This action is expected to reverberate across South Korea and globally, but it will encourage the implementation of stricter installation and safety regulations.

Outlook

Ireland is expected to initiate the first stages of the new ancillary services market, later this quarter. Between 91 and

140 MW are expected to be procured in September 2019, with all systems planned to be installed by September 2021.

Australian states and territories continue to support renewable energy generation and co-located battery systems, ahead of the federal election in May. South Australia has set the precedent for the other states, with generous energy storage subsidies. As some Australian territories have high residential electricity prices, IHS Markit expects PV system owners to explore storage opportunities, as regional governments encourage uptake of residential solar and storage, as well as the advancement of aggregated systems into virtual power plants (VPPs).

The U.S. Federal Energy Regulatory Commission (FERC) issued Order 841 in February 2018, which aims to remove key regulatory barriers for electrical energy storage and aims to create a level playing field for storage to access new revenue streams (e.g. wholesale markets). As of December 2018, Independent Systems Operators and Regional Transmission Organizations have all submitted plans reflecting the unique characteristics offered by energy storage resources, which will begin to be implemented in 2019.

This policy and regulatory developments mean 2019 should be another positive year for energy storage. Following a strong finish in 2018, greater geographic diversity, a more global supplier base advancing the industry, and new applications that are rapidly developing signify an optimistic outlook.

The views and opinions expressed in this article are the author’s own, and do not necessarily reflect those held by pv magazine.

The views and opinions expressed in this article are the author’s own, and do not necessarily reflect those held by pv magazine.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.