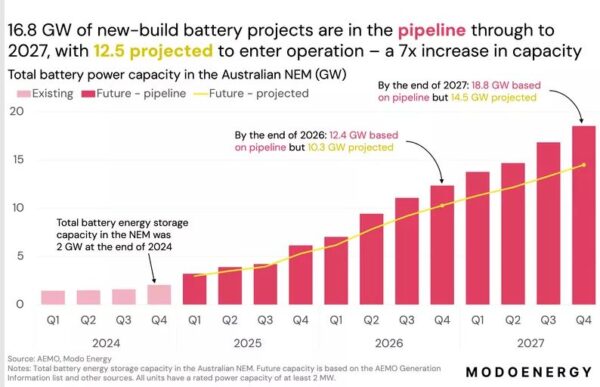

New data from Modo Energy shows 16.8 GW of new-build battery energy storage projects are being developed in the National Electricity Market (NEM) with the company projecting 12.5 GW of this pipeline will begin commercial operations in the next three years.

Modo Market Analyst Hatta Misra said grid-scale battery capacity in the NEM is expected to reach 14.5 GW by the end of 2027, a sevenfold increase on the 2 GW currently available on the grid.

Misra said the projections, detailed in the company’s latest NEM Battery Energy Storage Pipeline Report, are based on the development status of the individual projects.

“More than 6.2 GW of batteries are currently under construction or in commissioning, triple the power of the current operating fleet,” he said. “A further 4.6 GW of batteries in the pipeline have also reached financial closure or are in advanced planning stages.”

“This means that 10.9 GW of batteries are in advanced stages of development. We believe that these batteries will almost certainly be constructed and will likely be completed on schedule.”

Misra said another 5.6 GW of projects in the pipeline are in earlier planning stages or are still classed as tentative.

“These projects face a greater risk of delay, downsizing, or cancellation, and our projections of buildout reflect this risk,” he said.

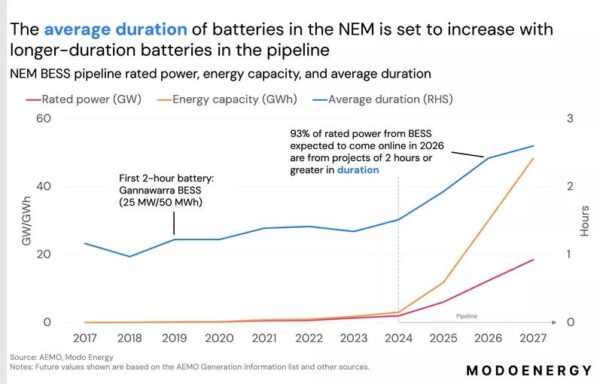

UK-headquartered Modo, which entered the Australian market last year, said the shift to bigger batteries in the NEM is a key driver of the expected capacity growth with 19 of the projects forecast to come online in the next three years 300 MW or larger.

Construction of some of these longer-duration batteries, including Origin Energy’s 700 MW / 2,800 MWh Eraring battery project being built on the New South Wales (NSW) Central Coast, and the 50 MW / 400 MWh Limondale battery being built by German energy utility RWE in that the state’s Riverina district, has already commenced.

The shift to longer-duration batteries is also expected to have a major bearing on total energy storage capacity with Misra confirming that most projects in the pipeline are at least two hours duration.

“Currently, batteries with durations of two hours or less dominate the 3 GWh of battery energy capacity in the NEM, with the average duration of the fleet being 1.5 hours,” he said. “However, based on the pipeline, the NEM will have over 40 GWh of energy capacity by the end of 2027, due to 95% of pipeline projects having durations of two hours or greater.”

Modo said the pipeline of battery projects is concentrated in New South Wales (NSW), Queensland, and Victoria. Of the 16.8 GW in the pipeline by the end of 2027, 6 GW are located in NSW, 4.8 GW in Queensland, and 3.9 GW in Victoria.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.