Why silver became the problem

Silver has been the default interconnection material in solar panels since the industry scaled commercially. It conducts well, prints reliably, and for a long time the economics were manageable.

That changed. Fast.

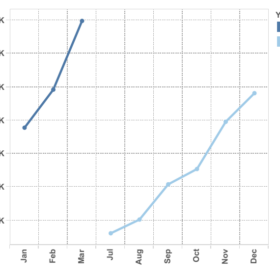

Supply and demand imbalances, compounded by tariff-driven market disruption, triggered a severe liquidity squeeze in the silver futures market through 2025. COMEX silver moved from $27.54 (USD 19.46) in early 2025 to a peak of $94.74 by January 2026, a 244% rise in under a year. [3]

For an industry that embeds silver paste into every solar cell it produces, this is not a pricing footnote. It is a structural manufacturing cost crisis.

Image: Comex

For manufacturers still reliant on silver paste, every panel shipped is a bet on precious metal availability and price stability. That bet is getting structurally harder to sustain.

Moving away from silver

The silver price shock has triggered a fundamental rethink across the manufacturing industry. Analysts project that silver intensity per watt must fall to approximately two milligrams per watt peak to sustain multi-terrawatt manufacturing long-term. [7]

In 2025 alone, multiple global producers of HJT and TOPCon modules announced programmes to reduce or eliminate silver paste, flagging silver in investor briefings and annual reports as a key input cost risk.

Research has been pointing to copper as the answer for years. Of the candidate materials, copper is the only one with the conductivity, mechanical strength, and abundance profile capable of replacing silver at the scale solar manufacturing now requires.

Germany’s Fraunhofer ISE demonstrated copper-metallised heterojunction cells achieving higher efficiency than conventional silver-contact reference cells at just 1.4 milligrams of silver per watt peak. [8]

The Netherlands’ TNO confirmed copper metallisation performance within 1% of silver-based cells using existing screen-printing equipment, removing the barrier of new capital investment. [9] The material conclusion from independent research is consistent: copper.

What stopped it happening sooner were three manufacturing barriers the industry had been unable to resolve at commercial scale.

The first was copper diffusion: copper atoms migrate into silicon under heat, forming recombination traps that degrade cell efficiency over time.

The second was adhesion: plated copper contacts showed unreliable bonding to cell surfaces under thermal cycling, a reliability concern that manufacturers producing 25-year warranted products could not accept.

The third, and most consequential, was the absence of a cost-effective selective deposition process. The semiconductor industry standard of photoresist coating and photolithography was technically capable but economically incompatible with the cost and throughput demands of solar manufacturing. [10]

These were the reasons copper metallisation remained a laboratory direction while the industry continued printing silver paste at scale, even as the supply trajectory became increasingly clear.

A different starting point: AIKO’s silver-free strategy

AIKO’s copper story does not begin in 2025 as a response to cost or supply pressure. It was the founding architectural decision of the company’s all-back-contact (ABC) cell design, an act of strategic vision and deliberate engineering innovation at a time when the rest of the industry had neither the incentive nor the ambition to question the silver standard.

The ABC architecture resolved the diffusion barrier structurally. With all electrical contacts on the rear of the cell, the copper-to-silicon diffusion risk is managed through cell geometry itself, removing the constraint that had blocked copper adoption in conventional front-contact designs.

The selective deposition barrier was resolved through AIKO’s proprietary laser patterning process. By using laser ablation to define contact regions before electroplating, AIKO achieved the precision of photolithography without its cost or complexity. Copper deposits exactly where required: no photoresist, no stripping, no semiconductor-grade tooling cost.

AIKO began R&D and pilot production of silver-free copper metallisation in 2021, with commercial ABC module production scaling from 2022 and full gigawatt-scale copper deployment from 2025.

More than 12 GW of copper-based modules have since been shipped globally, the first commercial proof that silver-free copper metallisation was not only technically viable but scalable at volume. The manufacturing constraint that had held the industry back was not worked around. It was solved.

What the decision delivers

The shift from silver paste to copper interconnects changes three things that directly affect the economics and performance of every installation.

Stable pricing and independence from silver volatility

Copper reserves are estimated at 980 million tonnes, more than 3,000 times greater than silver, [11] and trade on stable commodity markets. Module pricing tied to copper does not move because a precious metal had a difficult quarter. Installers quote with confidence. Customers are not exposed to price movements between the initial conversation and the signed contract.

Supply continuity

The 2025 silver crisis demonstrated the exposure that silver-dependent manufacturing carries. When futures markets seize and production costs spike, delivery timelines become unpredictable across the supply chain. Copper-based production operates independently of precious metal market conditions.

Measurably better performance, independently certified

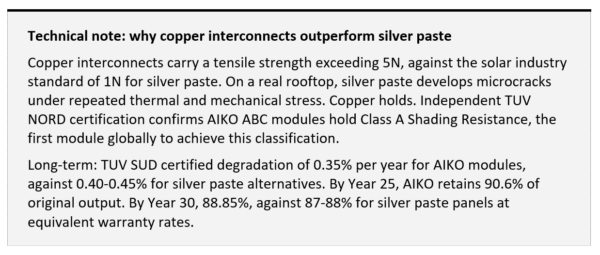

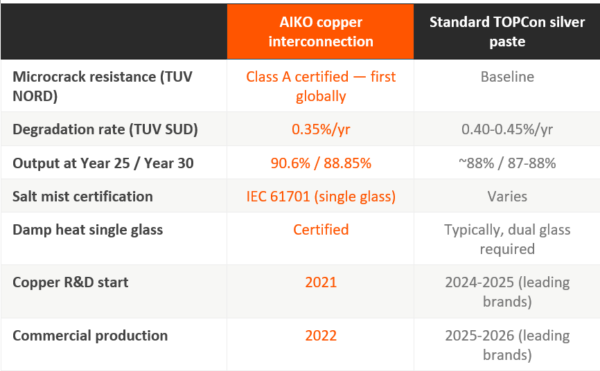

Independent TUV NORD certification confirms AIKO ABC modules hold Class A Shading Resistance, the first module globally to achieve this classification. TUV SUD certified long-term degradation of 0.35% per year for AIKO modules, [12] against 0.40 to 0.45% for silver paste alternatives.

By Year 25, AIKO retains 90.6% of original output; by Year 30, 88.85%, against 87 to 88% for silver paste panels. [13] At current grid electricity prices, that compounding difference represents thousands of dollars in generation revenue over the life of a system.

In coastal installations, copper’s resistance to salt-air oxidation removes a degradation pathway that silver paste cannot avoid. AIKO achieves IEC 61701 salt mist certification in single-glass construction, [14] without the dual-glass configuration that competing products typically require for equivalent coastal performance.

The ANZ policy dimension

The Australian Renewable Energy Agency (ARENA) ultra-low-cost solar agenda has consistently identified material efficiency, including silver intensity per watt, as a structural constraint on Australia’s ability to deploy solar at the scale the energy transition requires.

AIKO’s success in copper metallisation at gigawatt scale opens a path toward solar production that is not structurally constrained by precious metal supply or pricing volatility, directly relevant to that agenda. AIKO’s research partnership with ACAP and UNSW [15] further connects that commercial capability to the Australian scientific community.

For Australian investors, asset managers, and commercial and industrial (C&I) buyers evaluating long-term solar procurement, the silver supply question is increasingly a risk management question. Panels whose performance and pricing are structurally linked to a precious metal facing sustained demand pressure carry a different risk profile from copper-based alternatives.

Copper is one of the most abundant and most recycled industrial metals on earth, with global recovery rates exceeding 50% and established recycling infrastructure across Australia. As Australia’s installed solar base approaches its first significant wave of end-of-life, the material composition of those panels will determine how circular the energy transition actually proves to be.

Opening the path to a more resilient solar future

AIKO’s success in copper metallisation at gigawatt-scale production moves copper from a promising research direction to a demonstrated commercial reality, and with it, opens solar manufacturing to a more sustainable future less dependent on silver’s volatile supply and pricing. For customers, that translates into better performance, higher durability, and more stable cost.

The industry’s shift toward copper-based metallisation is a strong validation of the strategic and technical position AIKO established in 2021. That sequence reflects a company that has consistently oriented its R&D investment around where photovoltaic technology needed to go, rather than where prevailing economics pointed.

What remains to be seen is whether the rest of the industry follows with the same commitment, rebuilding cell architecture around copper to genuinely solve the problem, or settles for incremental silver reduction: enough to manage input costs, but not enough to deliver the performance and supply chain independence that a full transition makes possible.

Author: AIKO Solar

*

References

[1] TUV NORD independent certification. AIKO ABC modules hold Class A Shading Resistance, first module globally to achieve this classification. Mechanical stress performance data from AIKO technical testing, presented at SNEC 2024.

[2] TUV NORD independent certification. AIKO ABC modules hold Class A Shading Resistance, first module globally to achieve this classification. Mechanical stress performance data from AIKO technical testing, presented at SNEC 2024.

[3] COMEX silver futures price data. Low: $27.54/oz (March 2025). Peak: $94.74/oz (January 2026).

[4] Hallam et al. The silver learning curve for photovoltaics and projected silver demand for net-zero emissions by 2050. Progress in Photovoltaics: Research and Applications, 2023. doi:10.1002/pip.3661.

[5] The Silver Institute. Solar silver demand projections to 2030.

[6] Silver Institute, World Silver Survey 2024 (published April 2024). PV silver demand grew 64% to 193.5 Moz in 2023.

[7] Hallam et al. Design Considerations for Multi-terawatt Scale Manufacturing of Existing and Future Photovoltaic Technologies. Energy and Environmental Science, Royal Society of Chemistry, 2021. doi:10.1039/D1EE01288F.

[8] Fraunhofer ISE, April 2025. Reported in pv magazine and PV Europe, June 2025. 1.4mg/W silver consumption, copper paste on rear of HJT cells, achieving higher efficiency than silver reference cells.

[9] TNO Solar Energy Group. Presented at EUPVSEC, Bilbao, October 2025.

[10] Lennon et al. Challenges facing copper-plated metallisation for silicon photovoltaics. Progress in Photovoltaics: Research and Applications, 2019. doi:10.1002/pip.3062

[11] USGS Mineral Commodity Summaries 2024. Copper reserves: 980 Mt. Silver reserves: 0.27 Mt.

[12] TUV SUD long-term degradation certification. AIKO ABC module series, 2023.

[13] AIKO warranty: 90.6% output at Year 25, 88.85% at Year 30 (0.35%/yr from Year 2, TUV SUD certified). Standard silver paste panels warranted at 0.40-0.45%/yr project 87-88% at Year 30.

[14] IEC 61701 Salt Mist Corrosion Testing. TUV Rheinland certification PV50572634.

[15] Australian Centre for Advanced Photovoltaics (ACAP) / UNSW research partnership with AIKO.

The views and opinions expressed in this article are the author’s own, and do not necessarily reflect those held by pv magazine.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.