While PV tracking was deployed in 20% of PV power plants globally in 2017, in Australia the level of penetration was above 90%. This was one of the findings made by GTM Research in its latest tracker-market report.

“The tracker market in Australia exploded in 2017, exceeding 1.4 GW,” Scott Moskowitz, senior analyst at GTM Research and author of the study told pv magazine Australia.

“Trackers are obvious in Australia for the same reason they are obvious in the U.S. and Latin America. The market is sophisticated, [solar] insolation is extremely high, and the land is highly suitable to trackers,” added Moskowitz.

Tracker system suppliers use a range of different drive mechanisms to slowly rotate rows of PV modules across the day, to ensure they are at an optimal angle maximising exposure to the sun’s rays.

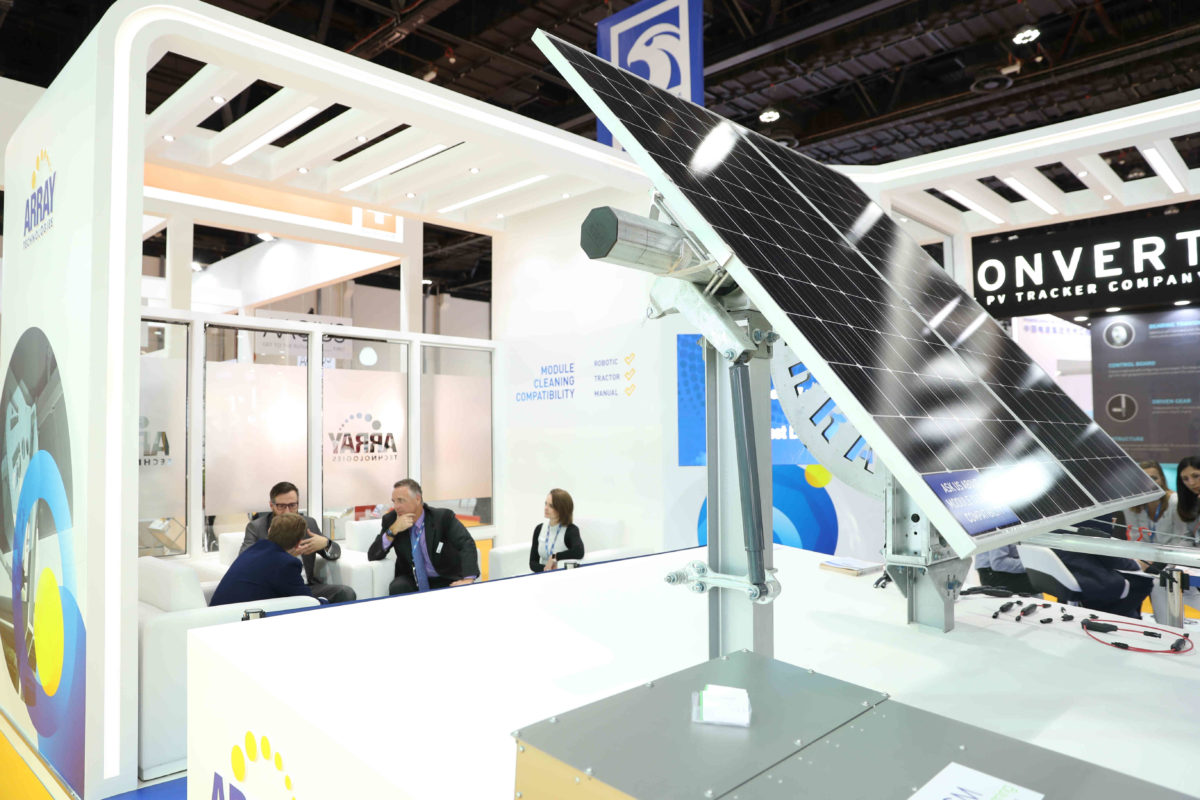

U.S.-based Array Technologies, while the number two supplier globally, is the leading supplier of trackers to the Australian market. Competitors Nextracker, ranked number one globally, NClave, and PV Hardware also have “a sizable presence” in the market, according to GTM.

![]()

Array deploys a centralized tracker architecture, with a linked, terrain-flexible rotating driveline moving many rows of modules, while Nextracker, a Silicon Valley spin-off, uses a decentralized architecture, with rows moving independently and powered by mini modules and battery packs.

Albuquerque-based Array has “strategically targeted” the Australian marketplace, GTM reports, having established a local sales and service presence.

While tracker deployment may be ‘no-brainer’ in the Australian PV marketplace, the wide range of climates, geographies and geologies across such a huge country brings with it technical challenges.

“There is no one-size-fits-all tracker and certain solutions work better depending on the slope of the land, the makeup of the soil, the prevalence of dust and soiling, and numerous other factors,” said Moskowitz.

Globally, tracker shipments grew 32% in 2017, down from highs of 254% growth in 2016. While this may seem like a disappointing result for tracker suppliers, declines in the U.S. market significantly depressed this figure. Moskowitz notes that if the U.S. market is discounted from its analysis, that global tracker shipments grew “an astonishing” 184%.

Moskowitz explains: “Shipment growth of 32% in 2017 is actually a significant achievement given that shipments in the United States, the country with the most tracker shipments in 2016 and 2017, fell 44% in 2017.” Tracker deployment is particularly attractive to U.S. project developers as the Investment Tax Credit for large scale solar is based on project capex – towards which a tracker system is a considerable component.

In “low-cost markets” such as China and India, tracker deployment is not as common. With China remaining the global dominate PV market, with over 50 GW installed across all market segments in 2017, penetration levels of around 20% in that country push down the global figure.

“We expect tracker penetrations in the U.S., Latin America, Middle East, and Australia markets to track upwards toward that 80 to 90% level, but the overall share of global installations with trackers will remain below 50% as long as China is the world’s largest solar market,” Moskowitz concludes.

This article was edited on March 1, 2018 to reflect that Array deploys a linked, rotating driveline rather than a push-pull actuator.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.