The Australian Energy Regulator’s (AER) latest Wholesale Markets Quarterly Report shows that rooftop solar generation reached record highs during the July to September quarter of 2023, helping to drive wholesale energy prices and demand levels to new lows.

The report shows average wholesale electricity prices in the National Electricity Market (NEM) were less than half that seen at the same time last year.

Electricity demand fell to its lowest level yet for a third quarter, averaging about 5%, or 1,200 MW, lower than the same period last year.

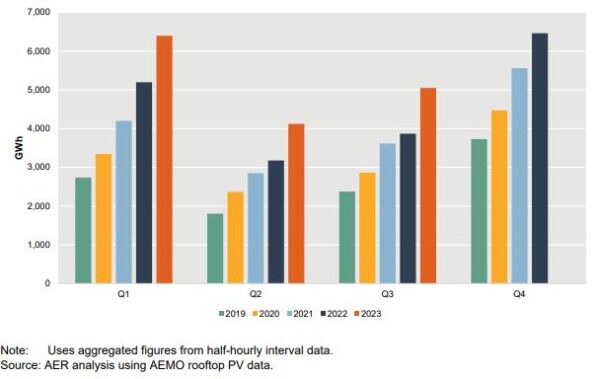

The AER said this was driven by mild weather conditions alongside a huge increase in rooftop solar output which was 31% higher than the same quarter last year, and in September alone was 41% up on a year ago.

Image: AER

With continued growth in rooftop solar installations, the regulator expects the record output from rooftop solar will likely be surpassed in the final quarter of 2023 but warned the roll out of large-scale renewable energy assets needs to accelerate to keep pace with the shift from a grid dominated by coal-fired generation.

Modelling by the Australian Energy Market Operator (AEMO) has forecast potential supply shortfalls for all mainland regions over the next 10 years with 8.3 GW of coal-fired generating capacity scheduled to exit the National Electricity Market (NEM) grid by 2030.

The AER said just two solar farms, two wind farms and two big batteries – which will constitute about 800 MW of capacity once fully commissioned – commenced generating in the NEM during the July to September quarter of 2023.

The regulator said more large-scale energy assets are needed to keep pace with the planned coal plant retirements over the next decade.

“Overall, the rate of new entry into the market is not in line with what the market needs to transition,” it said. “With 8.3 GW of firm capacity scheduled to exit the market in the next decade as coal plants retire, there is a pressing need for new investment to be realised across the NEM.”

Despite its concerns, the AER said the progressive connection of new solar farms meant there was more low-priced capacity in the NEM this quarter than either last quarter or in Q3 2022.

Compared to last quarter, an additional 1,500 MW was offered below $70 per MWh with large-scale solar generators, coal and hydro contributing most of the increase in low-priced capacity.

Average prices in the NEM ranged from $31 per MWh in Tasmania to $114 per MWh in South Australia, but prices this quarter were lower in all regions compared to the previous three months.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

1 comment

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.