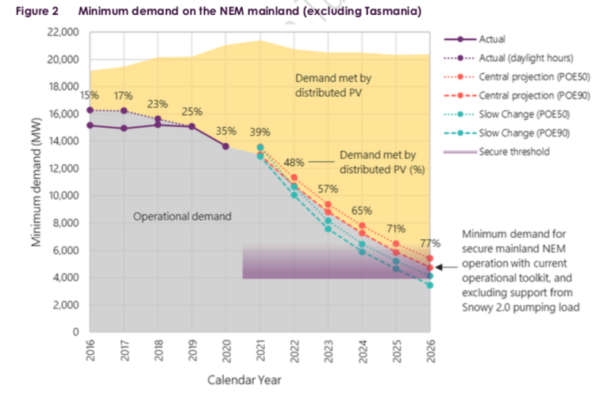

Solar in Australia could supply up to 77% of total electricity demand at times by 2026, the Australian Electricity Market Operator (AEMO) has revealed in its annual Electricity Statement of Opportunities report published today.

The report predicts new renewable energy generation and energy storage projects will be able to supply the country as coal-fired plants retire, contradicting concerns around reliability and supply shortfalls.

“No reliability gaps are forecast for the next five years, primarily due to more than 4.4 gigawatts (GW) of new generation and storage capacity, as well as transmission investment and reduced peak demand forecasts,” AEMO chief executive Daniel Westerman said. AEMO is also confident about the following five years to 2031, so long as proposed renewable generation, storage and transmission investments are actually committed.

In fact, AEMO has pointed to coal plant failures, like the flooding at Victorian’s Yallourn plant in June, as the most pressing reliability threat.

Rooftop solar soars, curbing demand

AEMO has bumped up its solar forecasts from last year and now estimates 8.9 GW of new distributed PV capacity will be installed by 2025. In addition to utility-scale solar plants, AEMO forecasts 6.5 GW of that capacity will come from commercial and residential solar installed in the NEM, which includes every state and territory except Western Australia and the Northern Territory.

With solar booming, focus has now shifted from fears of supply shortfalls to demand shortfalls, as more houses and businesses power themselves through their rooftop systems.

AEMO is expecting electricity demand in the main electricity market to drop to a record low of between 4 GW and 6 GW by 2025, down from 15 GW in 2019. This drop in minimum operational demand, which is happening even faster than last year’s predictions, has been flagged as a major threat to power system security, with AEMO noting the necessity for reforms as well as government policy to accelerate electrification of homes and transport, which would at least partially reverse the downward demand trend.

“Without additional operational tools, we may no longer be able to operate the mainland NEM securely in all periods from 2025 due to a lack of security services when demand from the grid is so low,” Westerman said. “These conditions may occur earlier than 2025 under abnormal network conditions, such as network and generation unit outages, possibly associated with bushfires or storms,” he added.

Westerman pointed to the Energy Security Board’s recent reform recommendations as addressing some of these issues. Despite delivering a suite of reforms around the integration of distributed energy resources like solar and batteries, headlines have been dominated by the proposal of a capacity market, which many fear the Morrison government will shape into a “coal-keeper” scheme.

WHOO MADEE THISSS?? #Auspol #CoalKeeper #Climate #COP26 #AngusTaylor pic.twitter.com/wK2meQpoix

— Dan Ilic (@danilic) August 27, 2021

Given the capacity market proposal seeks to solve the issue of reliability, the Clean Energy Council’s chief executive, Kane Thornton, said the mechanism seems “unjustified in light of the current reliability outlook”.

Coal out

Since AEMO’s report last year, a number of planned thermal generator retirements have been brought forward, including the Yallourn Power Station (now scheduled to close in 2028), one unit of Eraring Power Station (2030) as well as the mothballing of one unit of Torrens Island B Power Station expected in October.

If no additional dispatchable energy or transmission projects come into the market, these early closures could cause reliability gaps in Victoria and New South Wales from 2026 to 2031, AEMO said.

Australian Electricity Market Operator (AEMO)

While early closures have potential to be disruptive, AEMO pointed out that the coal plants themselves are a threat to reliability. “Coal-fired generation reliability remained at historically poor levels last year,” the report said.

“While some plant improvements are expected in the near term, most generators are anticipating a trend of decreasing reliability in the longer term, increasing supply scarcity risk. The accelerated exit of coal and growing risk of plant failures is increasing the need for dispatchable projects,” it added.

Opportunities

This shift away from thermal generation towards clean energy will require a range of new services, AEMO said. It is looking for the market to provide solutions like frequency control ancillary services (FCAS), fast frequency response (FFR) and recovery services, load shifting, and active management of distributed energy resources. Such services are increasingly being provided by big batteries as well as new inverter technologies, with rules currently being introduced to accelerate this.

Storage like batteries and pumped hydro are also increasingly important as solar shifting devices, “soaking” excess solar generation by storing it or having demand flexibility. The aim, AEMO said, is to restrict the curtailment of large and small scale solar systems to be a last resort.

Australia has seen a massive spike in storage projects with investors backing 650 MW of large-scale batteries this year alone, amounting to an annual increase of more than 400%. In fact, the pipeline of publicly announced storage projects, beyond those already operating and committed for operation, includes 21 GW of battery storage and 6.3 GW of medium to long-term duration storage.

Demand flexibility solutions could also be provided through new uses for electricity, AEMO said, including hydrogen production and electrification of industrial processes and transport.

Hydrogen in

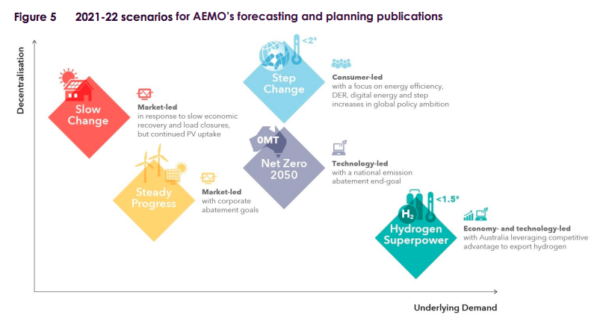

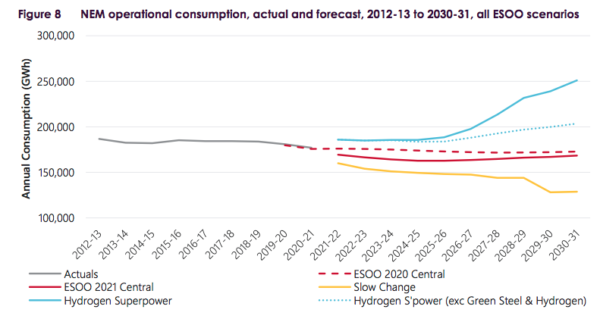

For the first time, AEMO has this year included green hydrogen as a scenario in its modelling. Named the “hydrogen superpower” scenario, it is the next progression from the ‘Step Change’ trajectory Australia is currently following.

“Momentum is building in the industry as the development of a hydrogen economy may simultaneously enable a significant new export opportunity and provide a means to achieve carbon emission reduction objectives,” AEMO’s report said. “There are now more than 10 projects at the 100+ MW scale being actively developed across Australia, and many more at a smaller scale.”

Electrification

AEMO has also considered a path called ‘Strong Electrification sensitivity’, in which case hydrogen uptake is limited and energy efficiency is also muted, leaving the majority of the emissions reductions to be achieved through electrification.

If there are strong incentives for electrification of transport, residential and industrial sectors, including heating, Australia could add almost 81 TWh of additional consumption by 2031. This is equivalent to 46% of total current operational consumption in the NEM.

“Beyond the next decade, the potential growth due to electrification, hydrogen production and associated zero-emissions industry is forecast to be even more significant, with NEM consumption potentially doubling by 2050,” the report added.

100% instantaneous renewable generation

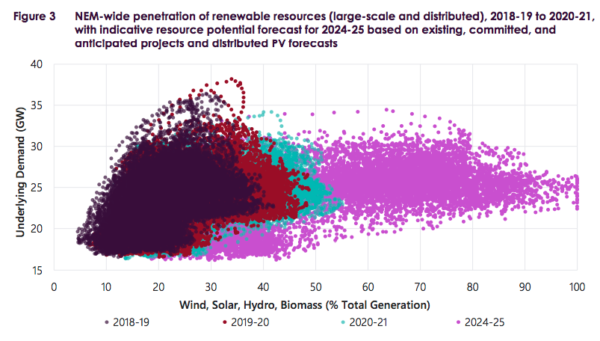

AEMO predicts if the current rate of large-scale wind and solar development continues, there could be sufficient renewable resources available in 2025 to meet 100% of underlying consumer demand in certain periods.

In July, Westerman announced AEMO is readying Australia’s grid for such instances, eager to end the curtailment of clean energy assets which have plagued Australia’s landscape. This is a decisive shift away from the traditionally favoured thermal generators, which are difficult and slow to ramp up and down, towards what Westerman calls “zero-cost renewables”.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

1 comment

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.