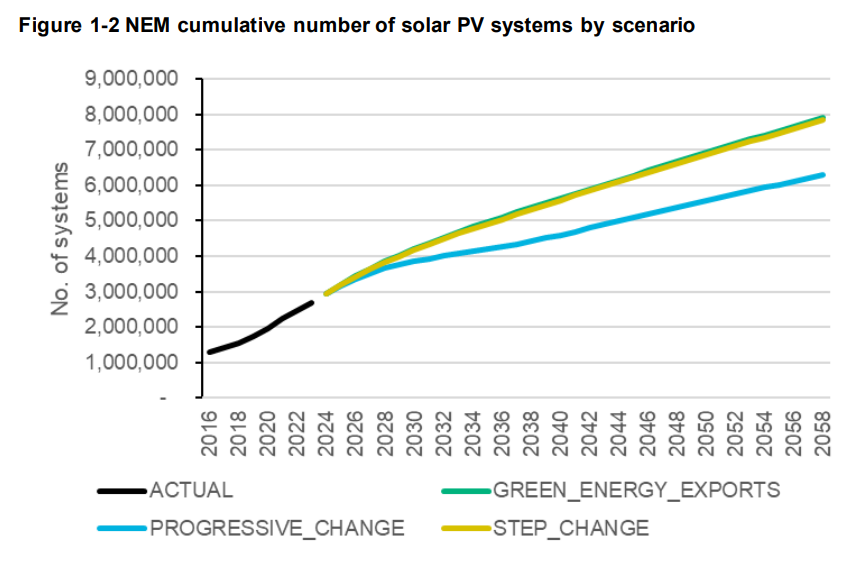

GEM’s December 2023 report found rooftop PV installation forecasts surpass current 41 GW levels of installed capacity in the NEM for coal, gas and hydro combined, but varies dependent on the government’s three decarbonisation scenarios.

These scenarios are Progressive Change, Step Change and Green Energy Exports. Progressive Change would see 43% emissions reduction by 2030 and net zero by 2050. The Step Change scenario is based on consumer driven investment to maintain temperature below 2 C. While Green Energy Exports foresees a limiting of temperature increase to 1.5 C, requiring rapid electrification, green hydrogen production, and bio-methane solutions.

The Projections for distributed resources – solar PV and stationary energy battery systems report found under the Progressive Change model, a capacity by 2053/54 of 66 GW, which is higher than CSIRO’s projection used by AEMO for the same period, of 48 GW.

Forecasts for the globally favoured models, Step Change and Green Energy Exports, landed on a 98 GW capacity from Green Energy Markets projections, and 92 GW from CSIRO.

“No matter which way we cut this, these forecasts indicate we are headed for an amount of rooftop solar capacity (taking into account panel degradation) that is close to, or greater than typical average electricity demand,” Tristan Edis, the director of Analysis and Advisory at Green Energy Markets and co-author of the report.

“Then on top of this we also have solar capacity in solar farms and large commercial installation above 100 kilowatts per system. For many, such a large amount of rooftop solar capacity seems to stretch the boundaries of credibility.”

Edis says there are four reasons to install more rooftop solar capacity than typical total electricity demand across residential customers, but every sector of the economy as well.

“Over time, given that solar panels can last 20 years, we end up with a steady accumulation of more and more capacity, even though overall the number of new sites installing solar each year is expected to decline substantially from what we’ve experience in the last few years,” Edis said.

As capacity grows and curtailment ensues, and the value of solar generation in the wholesale electricity market, along with feed-in tariffs declines, Edis said the caveat is heavily contingent on the price of home battery storage systems declining too.

Thirdly, Edis reasons that despite common beliefs, distribution networks do have demonstrated capability to manage very high levels of household solar adoption with scope to better manage voltage at modest cost to integrate solar capacity.

“When you examine data on the proportion of households with solar by postcode in Australia, you find that distribution networks are already managing to handle geographic areas with very high concentrations of solar system adoption. In addition, in the future once batteries become attractively priced and widespread, this will substantially mitigate the voltage rise created by solar,” Edis said.

Capacity growth of household solar systems increased 380% from 2011 to 2021 when a then, record amount of STC-registered rooftop solar capacity of 3.2 GW was installed. However, Edis continued, the number of individual solar systems installed in that period was only up by 5% as the dominant driver of capacity growth was bigger systems, not more installations.

“Rooftop solar capacity is likely to accumulate over time to reach levels that dominate the electricity market, it doesn’t mean it will necessarily grow at the speed governments ideally need it to in order to achieve their emission reduction goals.

“Given the long lead times we are currently confronting with the build out of large utility-scale renewable energy projects, rooftop solar – which will need to be coupled with batteries – becomes especially important in helping Governments maintain progress towards their emission reduction goals.”

“However, it is very far from given that we will follow the Step Change or Green Energy Export trajectory of growth. Stakeholders need to recognise that these scenarios are intended to represent a very large scale-up in the rate of emission reduction effort in this country.

“Our own modelling has assumed a range of new government policies would be introduced, which we are yet to actually see implemented,” Edis said.

The report was co-authored with GEM founder Ric Brazzale.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

2 comments

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.