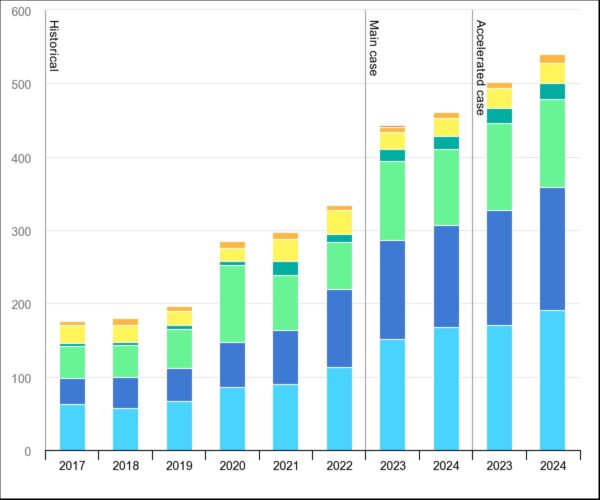

The International Energy Agency (IEA) says global additions of renewable power capacity are expected to surge by 107 GW to reach 440 GW in 2023, the largest annual addition yet. The figure represents about one third more renewable energy than the world added the previous year.

Overall, cumulative world renewable capacity is forecast to reach 4,500 GW at the end of 2024, equivalent to the total power output of China and the United States combined, as growing policy momentum, higher fossil fuel prices and energy security concerns drive strong deployment of solar and wind power.

“The global energy crisis has shown renewables are critical for making energy supplies not just cleaner but also more secure and affordable,” IEA Executive Director Fatih Birol said.

“Governments are responding with efforts to deploy them faster. This year, the world is set to add a record-breaking amount of renewables to electricity systems – more than the total power capacity of Germany and Spain combined.”

Overall global renewable energy capacity additions rose by almost 13% to nearly 340 GW in 2022 with solar responsible for nearly 220 GW, up 35% from 2021.

Image: IEA

In its Renewable Energy Market Update, the IEA says solar remains the main source of global renewable capacity expansion in 2023, accounting for 65% of growth. The agency said distributed applications, including commercial and residential rooftop systems, account for almost half of all global PV expansion.

Annual PV market growth is expected to continue, reaching almost 310 GW in 2024, with declining module prices, greater uptake of distributed solar systems and a policy push for large-scale deployment driving higher annual solar additions in all major markets. The IEA said these factors are outweighing rising interest rates, higher investment costs and persistent supply chain challenges.

The IEA said the market conditions had “created a favourable environment for solar PV, especially for residential and commercial systems that can be rapidly installed to meet growing demand for renewable energy.”

“These smaller distributed PV applications are on track to account for half of this year’s overall deployment of solar PV, larger than the total deployment of onshore wind over the same period,” the agency said.

While the IEA has predicted global renewable capacity additions will reach 440 GW in 2023, in one scenario it has estimated that additions could reach more than 500 GW this year.

The agency said reaching this level would depend on “the pace of permitting, construction and timely grid connection of projects under development.”

“Achieving stronger growth means addressing some key challenges,” Birol said. “Policies need to adapt to changing market conditions, and we need to upgrade and expand power grids to ensure we can take full advantage of solar and wind’s huge potential.”

The IEA said electricity generation costs from new onshore wind and PV plants are projected to decline by 2024 but will likely remain 10-15% above their pre-Covid levels in most markets outside China. Although commodity and freight prices have dropped from last year’s peaks, they remain elevated. At the same time, developers’ financing costs have increased due to rising interest rates. Despite this, the IEA said solar and onshore wind remain the lowest cost options for new electricity generation in most countries.

Global manufacturing capacity for all PV production segments is expected to more than double to 1,000 GW by 2024, led by China and increasing supply diversification in the United States, India and Europe.

While supply chains are diversifying, China’s contribution to global renewable capacity additions is expected to increase in 2023 and 2024, consolidating its position as the undisputed leader in global deployment.

In 2022, China accounted for almost half of all new renewable power capacity worldwide. By 2024, the country is expected to deliver 50% of all new solar PV projects globally, as well as almost 70% of all new offshore wind projects and more than 60% of onshore wind projects.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

3 comments

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.